News » An Ambitious FP9 Strengthening Europe’s Industrial Leadership

An Ambitious FP9 Strengthening Europe’s Industrial Leadership

Downloads and links

Recent updates

The participation of both Industry and Research and Technology Organisations (RTOs) in EU R&I Framework Programmes is essential to turn ideas into impact-driven and value-creating technologies, applications, and solutions. Among others, the engagement of the whole innovation ecosystem is supported by the contractual Public Private Partnerships (cPPPs) and Joint Technology Initiatives (JTIs). These instruments are one way to address private sector participation bringing leverage from industry.

Industry and RTOs are highly committed to the Societal Challenges and the Industrial Leadership pillars. Both should be strengthened to speed up efforts in overcoming the valley of death as well as the gap between the demonstration and commercialization phases. Contractual PPPs and the JTIs are unique platforms, which foster cooperation between public and private actors by pooling their diverse capabilities and creating the critical mass for innovative breakthrough. They also leverage the necessary funds for large-scale European projects. Understanding the channels to market as well as the challenges to upscaling, industry bridge gaps and accelerate the generation of impact and results from R&I programmes.

Download files or visit links related to this content

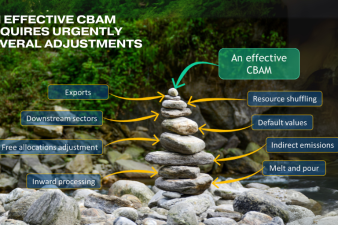

Brussels, 13 February 2025 – Following the high-level conference “A Carbon Border Adjustment Mechanism for Climate - Addressing carbon leakage to strengthen global climate action”, organised in Paris by the European Commission and the French Ministries of Finance, Economics and Climate Transition, EUROFER emphasises that simplification must go hand in hand with ensuring the instrument’s effectiveness. This means addressing key issues such as resource shuffling, exports, and the inclusions of products further down the value chain.

Brussels, 11 February 2025

Brussels, 06 February 2025 – The economic and geopolitical conditions that have affected the European steel market over the past two years show no signs of improvement and have further deepened their negative impact on the sector in 2024. Growing uncertainty continues to weigh also on 2025 and 2026, with the outlook hinging on unpredictable developments especially as regards international trade. According to EUROFER’s latest Economic and Steel Market Outlook, the recession in apparent steel consumption in 2024 will be steeper than previously projected (-2.3%, down from -1.8%) and the expected recovery in 2025 has now been downgraded (+2.2%, down from +3.8%). Similarly, steel-using sectors’ recession has been revised downwards for 2024 (-3.3% from -2.7%), while growth projections for 2025 have also been lowered (+0,9% from +1.6%). Some acceleration is not expected until 2026 (+2.1%). Steel imports remain at historically high levels (28%) also in the third quarter of 2024.

The European Steel Association (EUROFER)

172 Avenue de Cortenbergh

1000 Brussels

Belgium

Email: mail@eurofer.eu

Phone: +32 (0) 2 738 79 20