Publications » Position papers » Commission proposal on the revision of the Industrial Emissions Directive

Commission proposal on the revision of the Industrial Emissions Directive

Downloads and links

Recent updates

EUROFER members are firmly committed to significantly invest in the transition towards a clean, low-carbon future, in line with the Green Deal objectives. To this end, there is one investment cycle left to make the right decisions while keeping the EU steel industry competitive.

The transition of industry, and in particular the steel sector, will take place in stages: new plants will be built, new processes will be introduced and existing plants will continue to operate until the new plants/processes can replace them completely. An innovation-friendly environment with legal and planning certainty is necessary for the economic activities and the preservation of the competitiveness of the steel industry.

The existing IED has been a very effective tool for reducing industrial emissions and recent BREF reviews show that it is fit-for-purpose for addressing existing and future environmental challenges. For the industries to carry on with their transition, a consistent (respect the integrated approach), efficient (by accelerating permit procedures without unnecessary burden) and legally secure permit process is key.

However, it seems that IED review (IED 2.0) will lose its spirit and the BAT process will get a very new and not desired meaning. The Commission proposal makes us extremely concerned and, if no deletions or significantly amended, it will have the opposite effect. This paper concludes on the most important parts and EUROFER has elaborated plenty of proposals for the revised IED so it remains efficient whilst supporting innovation.

EUROFER key messages and requests

- Safeguarding the integrated approach to pollution prevention and control: the assessment of the well performing plants applying BAT(s) shows that availability of techniques is not given and that no installation in Europe can comply with the lowest end of range of all BAT- AELs defined in all the steel related BREFs as proposed by default in Art 15.3.

- BAT-AEPLs (raw material, water and energy) should remain non-binding to avoid hindering innovation as well as efficiency measures, but also ambitions for circularity. Therefore Art 15.3a should be deleted and Art 9.2 on energy efficiency measures maintained.

- IED 2.0 supports decarbonisation but need specific provisions for sectors under deep transformation like steel in an effective manner preventing large investments on existing assets that are planned to be phased, since the transformation would already be extremely capital intensive. Lately, the Seville process also contributes with the identification of de-C techniques and therefore, the Commission’s proposal to maintain Art 9.1 is supported.

- Accompany the transformation, not overloading neither micromanaging it:

- The EMS is already included in legally binding BAT conclusions (BREFs). The proposed Article 14a on EMS should be deleted.

- Emerging and innovative techniques are not at a level of maturity which allows a thorough data collection and establishment of the corresponding AELs – one of the underlying principles to develop BREFs/BAT conclusions. The revised IED should provide operators with sufficient time and a clear and solid legal framework to demonstrate that the expected performance of Emerging Techniques and the associated emission levels (ET-AELs) can be achieved in operational installations as well as legal certainty on what would happen should the expected levels not be achieved. Art. 27 c must be amended.

- Transformation Plans (TPs) should remain indicative: they should not be part of the permitting process nor have a binding character as these will be based on a number of parameters and key factors that are beyond the control of plant operators. We therefore ask that provisions (Article 27d) on TPs are deleted.

- Providing legal certainty to operators: BREF/BAT produced under the current IED must be regulated under the existing regime and not under IED 2.0, as BAT-AE(P)Ls have been produced considering the existing BREF guidance. An amended transposition article is needed.

- The publication of permits and company data must guarantee the protection of sensitive data against the background of competition rules (Article 13(b)2).

- In relation to Environmental Quality standards (EQS), competent authorities are invited to apply the principle of proportionality and adopt measures that will ensure that other sources will also reduce their specific contribution to the observed exceedance (Art 18).

- Exclude sectors of lower environmental relevance: the inclusion of cold rolling mills, wire drawing, smitheries with forging presses and small hammer smitheries mills (Annex I 2.3) is rejected.

The full text of the position paper on the revision of the Industrial Emissions Directive is available below.

Download this publication or visit associated links

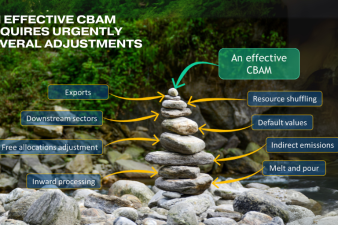

Brussels, 13 February 2025 – Following the high-level conference “A Carbon Border Adjustment Mechanism for Climate - Addressing carbon leakage to strengthen global climate action”, organised in Paris by the European Commission and the French Ministries of Finance, Economics and Climate Transition, EUROFER emphasises that simplification must go hand in hand with ensuring the instrument’s effectiveness. This means addressing key issues such as resource shuffling, exports, and the inclusions of products further down the value chain.

Brussels, 11 February 2025

Brussels, 06 February 2025 – The economic and geopolitical conditions that have affected the European steel market over the past two years show no signs of improvement and have further deepened their negative impact on the sector in 2024. Growing uncertainty continues to weigh also on 2025 and 2026, with the outlook hinging on unpredictable developments especially as regards international trade. According to EUROFER’s latest Economic and Steel Market Outlook, the recession in apparent steel consumption in 2024 will be steeper than previously projected (-2.3%, down from -1.8%) and the expected recovery in 2025 has now been downgraded (+2.2%, down from +3.8%). Similarly, steel-using sectors’ recession has been revised downwards for 2024 (-3.3% from -2.7%), while growth projections for 2025 have also been lowered (+0,9% from +1.6%). Some acceleration is not expected until 2026 (+2.1%). Steel imports remain at historically high levels (28%) also in the third quarter of 2024.

The European Steel Association (EUROFER)

172 Avenue de Cortenbergh

1000 Brussels

Belgium

Email: mail@eurofer.eu

Phone: +32 (0) 2 738 79 20